CTrader

The CTrader component enables users to submit and manage orders on the exchange. This module interfaces with the

Limit Order Book functionality provided by view_book & get_quote. Through this library users should

be able to quickly develop production ready algorithms.

Setup & The Ledger

In this library we have packaged a ledger object alongside the client such that building and calling complex, tick-accurate execution

algorithms is a simple process. Setting up these two objects is necessary when creating the enviornment to run the modules.

In order to build the ledger one needs to pass a list of symbols in String format however it is not necessary to use the ledger when using orders it just makes the process easier.

client = CSuite.connect_client(filename)

ledger = CSUite.build_ledger(client, symbols)

Orders & Order Entry

The Order Engine

In certain cases it may be necessary that the order generation and submission is contained by a recording and managment object, in this case, that is the Order Engine.

As an object, it contains the client, symbol and, ledger` (see above) and can be used to expedite and manage order submission and execusion processes for users necessitating a more streamlined interface.

Setting up the Engine:

engine = OrderEngine(client, symbol, ledger)

Building an Order:

order = engine.order(type, size)

Submitting the Order:

order.submit()

Warning

Iceberg orders are currently not supported

Limit Order

A limit order is a type of order to purchase or sell a security at a specified price or better. By using a buy limit order, the investor is guaranteed to pay that price or less. While the price is guaranteed, the filling of the order is not, and limit orders will not be executed unless the security price meets the order qualifications. If the asset does not reach the specified price, the order is not filled.

Limit Orders requires 6 parameters, the client for data access and 4 order parameters. In limit orders a Limit Price (Price) is necessary

and so is a symbol (str) and the quatity, which is also used to specify trade direction, e.g. +10 (BUY) and -10 (SELL).

The timeInForce variable specifies the order enforcment and defualts to Good-Till-Cancel (‘GTC’), it can be set to:

Good-Till-Cancel (‘GTC’): An order to buy or sell a security that lasts until the order is completed or canceled.

Fill-Or-Kill (‘FOK’): An order to buy or sell a security that must be executed immediately in its entirety; otherwise, the entire order will be cancelled.

Immediate-Or-Cancel (‘IOC’): An order to buy or sell a security that must be executed immediately. Any portion of an IOC order that cannot be filled immediately will be cancelled.

Limit Order support a stop through the stop parameter which has a defualt value of 0. The stop is set as a nominal (price) value which is automatically

converted into a TP or SL. For example passing a price of 100 and a stop of 120 would imply a Take Profit (TP), conversly a stop of 80 would imply a Stop Loss (SL)

Name |

Type |

Example |

Default |

client |

Client |

None |

None |

Price |

Float |

0.5002 |

None |

Size (Qty) |

Float |

15 or -50 |

None |

Symbol |

String |

‘BTCUSDT’ |

None |

stop |

Float |

0, 1.25 |

0 |

timeInForce |

String |

‘GTC’ ‘FOK’ |

‘GTC’ |

One can generate a simply Limit Order as such. For example to build an order for 1 BNB token at 0 with no SL/TP and a ‘GTC’ time parameter.

order = CSuite.LimitOrder(client, 300.0, 1, 'BNBUSDT', 0, 'GTC')

Note

These methods are available across all order types (LMT, MKT, PST)

Submit

To submit a built order to the Binance Exchange the submit method of the Limit Order can be used. It returns a filled order object with a

specified status and orderId.

sent_order = order.submit()

Requires: None

Returns: obj: order

Test

To validate a built order by submitting an identical test order the test() method may be used. This is useful if order parameters must be verified fast

as the call and response takes a mere 200ms. test() routes the order through the Exchange filters but not to the matchine engine.

If the order is valid a ‘{}’ is returned.

test_order = order.test()

Requires: None

Returns: API response string

Cancel

To cancel a submitted order (one that has recived a valid orderId variable) the cancel method can be used. This method returns the API response

string.

status = order.cancel()

Requires: None

Returns: order status string

Verify

This

Market Order

A market order is an instruction by an investor to a broker to buy or sell stock shares, bonds, or other assets at the best available price in the current financial market. It is the default choice for buying and selling for most investors most of the time.That means that a market order will be completed nearly instantaneously at a price very close to the latest posted price that the investor can see.

Market Orders requires 4 parameters, the client for data access and 3 order parameters. In Market Orders passing a price is not necessary

and however a so is a symbol (str) and quatity must be set, with the latter being used to specify trade direction, e.g. +10 (BUY) and -10 (SELL).

The timeInForce parameter is not necessary as all Market Orders are flagged for immedate execution.

Market Order supports a stop through the stop parameter which has a defualt value of 0. The stop is set as a nominal (price) value which is automatically

converted into a TP or SL. For example passing a price of 100 and a stop of 120 would imply a Take Profit (TP), conversly a stop of 80 would imply a Stop Loss (SL)

Name |

Type |

Example |

Default |

client |

Client |

None |

None |

Size (Qty) |

Float |

15 or -50 |

None |

Symbol |

String |

‘BTCUSDT’ |

None |

stop |

Float |

0, 1.25 |

0 |

One can generate a simple Market Order as such. For example to build an order for 1 BNB token with no SL/TP.

order = CSuite.MarketOrder(client, 1, 'BNBUSDT', 0')

Post-Only Order

A Post-Only order is a Limit Order which cannot be crossed with resting liquidity on the book, it can only cross against Market Orders thus, ensuring that the order is treated as a Maker order.

Post-Only Orders requires 5 parameters, the client for data access and 4 order parameters. In Limit orders passing a price is necessary

and however a so is a symbol (str) and quatity must be set, with the latter being used to specify trade direction, e.g. +10 (BUY) and -10 (SELL).

The timeInForce parameter is necessary but set to ‘GTC’ as defualt.

Post-Only Orders do not support a stop through the stop.

Name |

Type |

Example |

Default |

client |

Client |

None |

None |

Size (Qty) |

Float |

15 or -50 |

None |

Symbol |

String |

‘BTCUSDT’ |

None |

stop |

Float |

0, 1.25 |

0 |

One can generate a simple Market Order as such. For example to build an order for 1 BNB token with no SL/TP.

order = CSuite.MarketOrder(client, 1, 'BNBUSDT', 0')

Order Book Functions

Build Ledger

ledger = build_ledger(client, symbols)

This function recives and formats exchange information for a list of tradable tokens on the exchange. The ledger may be used to help pass variables into execution algorithms.

Requires: obj: client, arr of str: symbols

Returns: Pandas DataFrame

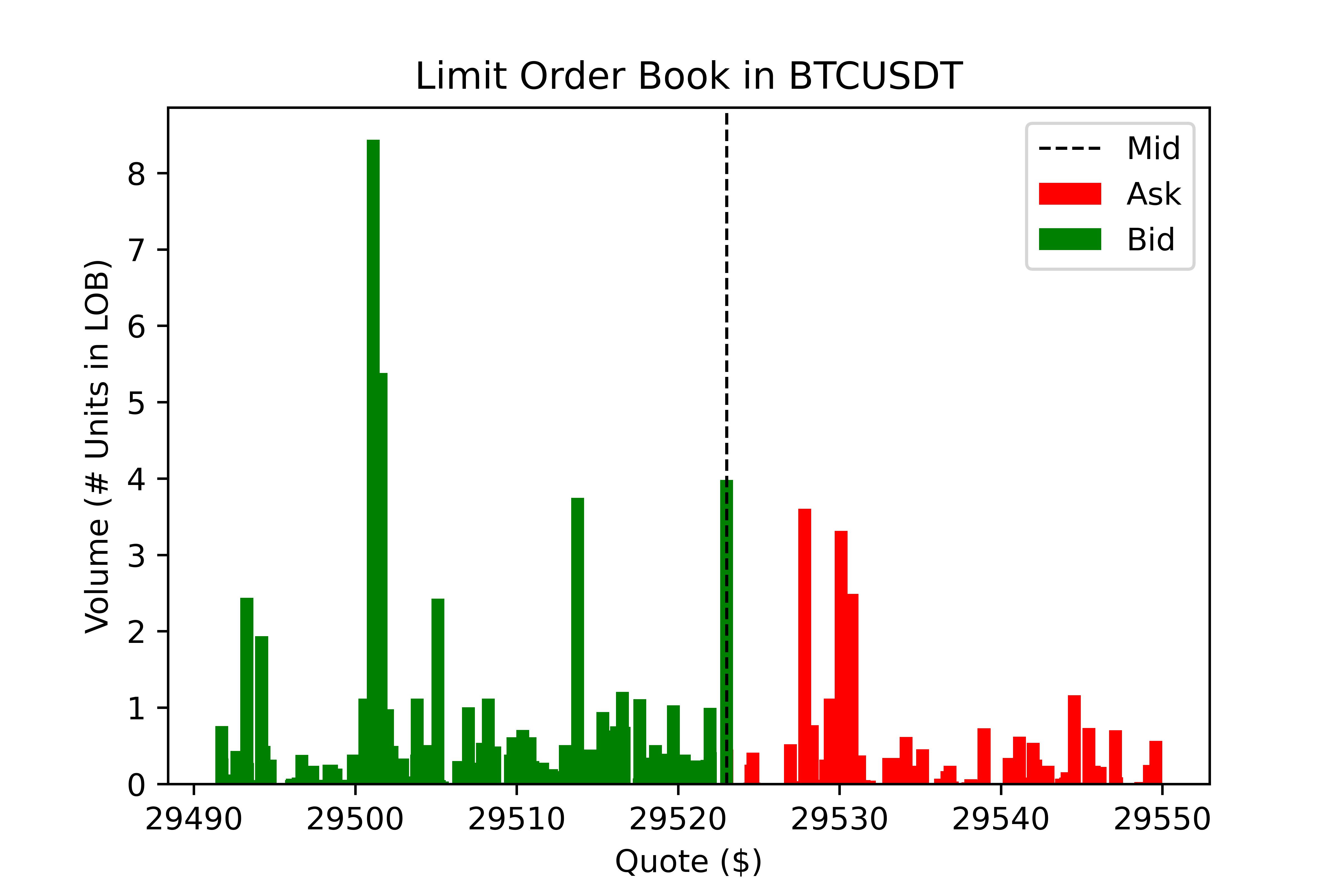

Plot Limit Order Book

This function allows users to quickly plot the current Limit Order Book (LOB) at a specified depth (limit).

Requires: obj: book, str: symbol, int: limit, bool: plot, bool: save, str: path

Returns: obj: book & plots plt

Expected Sweep Cost

esc = sweep_cost(book, size, symbol, side, ref)

This method returns the expected cost of sweeping the book with a specified size block. It requires a book object which is the first (indx: 0)

in the values returned by view_book, the size of the block order,

the symbol is for display purposes while the side specifies whether it is a ‘BUY’ or ‘SELL’ order. The ref parameter specifies the

starting reference price, for which are three options:

Bid (‘B’): Start at the best bid, calculates aggresive sells or passive buys.

Mid (‘M’): Start at the mid-point of the spread.

Ask (‘A’): Start at the best ask, calculates aggresive buys or passive sells.

Requires: obj: book, float: size, str: symbol, str: side, str: ref

Returns: Pandas DataFrame

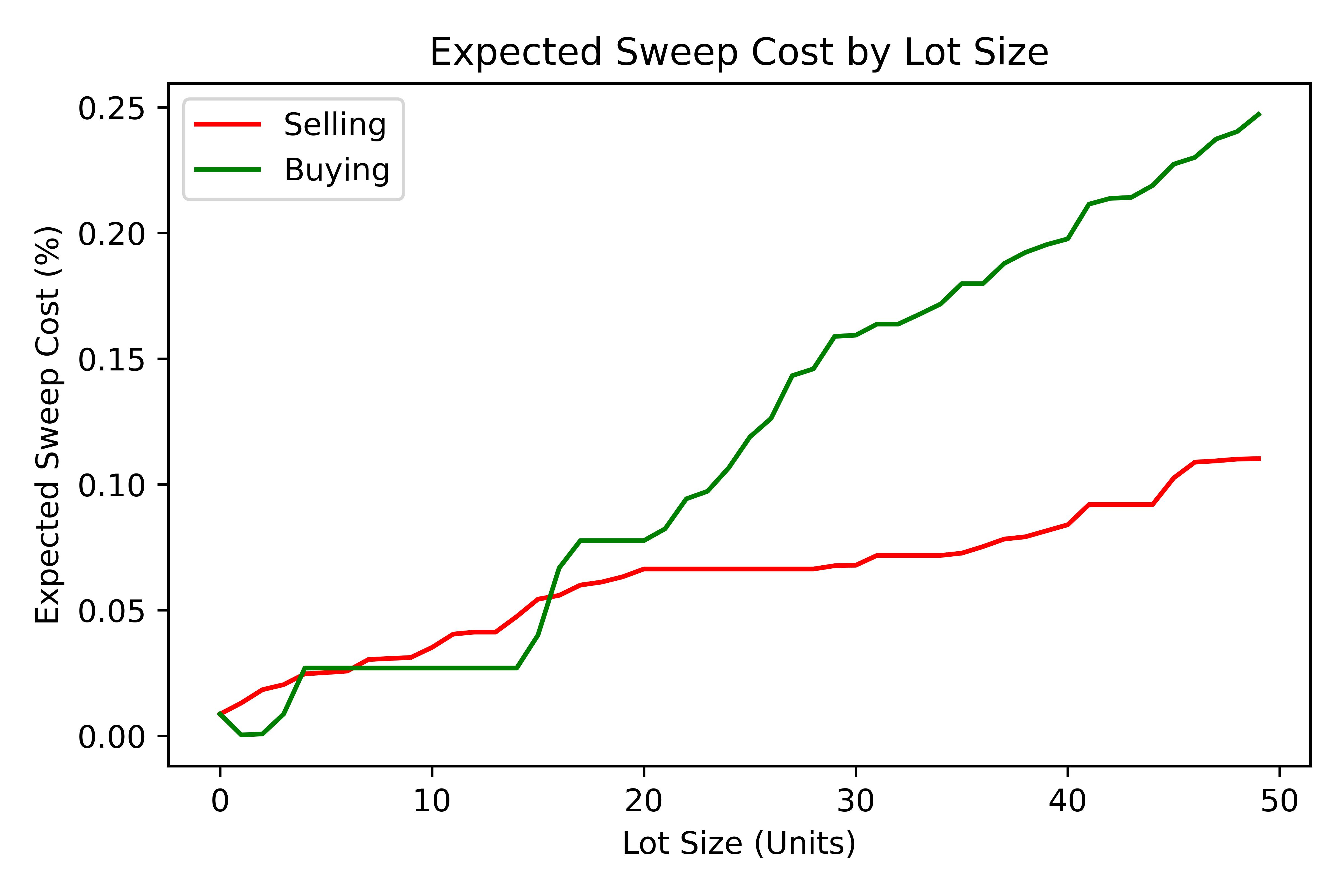

Plot Expected Sweep Cost

This function utilises the Expected Sweep Cost (ESC) function above in order to calculate the cost of different sized blocks. This returns a plot which provides insight into the depth of the LOB and cost of large transactions.

Requires: obj: book, str: symbol, int: max, int: inc, bool: plot, bool: save, str: path

Returns: None

Order Execution Algorithms

Utilising the extensive wrapping of functionality we can provide packaged execution algorithms which can

be worked with or without the OrderEngine

Tick Match

Tick Match (or Peg Match) is a propriatery high-speed, high-fill peg algorithm that requires no counterparty

(i.e. executes in the market). Tick Match enables the trader to peg an order at a specific tick distance from the BBO.

The algorithm executes by posting Limit Orders at a set distance from the BBO, say 2 or 3 ticks. Continous monitoring of

each order is the defualt and the time until the order is force cancelled is set via the refresh parameter. Each refresh cycle is

approx. 600ms.

Parameters

Name |

Type |

Example |

Default |

Decription |

client |

Client |

Object |

None |

API client |

symbol |

String |

‘BTCUSDT’ |

None |

Binance symbol str |

size (qty) |

Float |

0, 1.25 |

0 |

Order qty (neg = sell) |

tickSize |

Float |

0.0001 |

0 |

min tradable tick |

distance |

int |

1, 12 |

5 |

tick distance from BBO |

retry |

int |

5, 25 |

10 |

num of order submissions |

refresh |

int |

1, 3 |

1 |

num of monitor cycles |

Returns

Execution algorithms generally return an execution record comprised out of the BBO at execution time coupled with the orderId.

Direct Access

execution = CSUite.tick_match(client, symbol='BNBUSDT', size=1, tickSize=0.001, distance=3, retry=10, refresh=2)

Example code for running the algo to buy 1 ‘BNB’ token by sending 10 consecutive orders each at 3 ticks from the BBO. Furthermore, each order is monitored twice (specified via refresh) before forced cancelled if not filled.

via OrderEngine Wrapper

engine = OrderEngine(client, 'BTCUSDT', ledger)

execution = engine.tick_match(size=0.02, distance=3, retry=10, refresh=1)

Mid-Point Match

Mid-Point Market is a propriatery neutral high-fill rate algorithm designed for immediate execution in mean-reversion strategies. This algorithm posts aggressive limit orders at the mid-point (if it exists) or the best side BBO - i.e. if buy then best bid, if sell then best ask.

Name |

Type |

Example |

Default |

Decription |

client |

Client |

Object |

None |

API client |

symbol |

String |

‘BTCUSDT’ |

None |

Binance symbol str |

size (qty) |

Float |

0, 1.25 |

0 |

Order qty (neg = sell) |

tickSize |

Float |

0.0001 |

0 |

min tradable tick |

retry |

int |

5, 25 |

10 |

num of order submissions |

Direct Access

execution = CSUite.midpoint_match(client, symbol, size, tickSize, retry)

via OrderEngine Wrapper

engine = OrderEngine(client, 'ADAUSDT', ledger)

execution = engine.midpoint_match(size=50, retry=10)

Mini-Lot

Mini-Lot is a special excution algorithm dealing in mini-lots (i.e. lots close as possible to the minNotiona). It places Immediate-Or-Cancel (IOC)

orders at the BBO without crossing the spread, acting somewhat passively. This algorithm may be used to immediately acquire small quantities either to run small

systematic trading accounts, or

Name |

Type |

Example |

Default |

Decription |

client |

Client |

Object |

None |

API client |

symbol |

String |

‘BTCUSDT’ |

None |

Binance symbol str |

size (qty) |

Float |

0, 1.25 |

0 |

Order qty (neg = sell) |

tickSize |

Float |

0.001 |

0 |

min tradable tick |

stepSize |

Float |

0.1 |

0.1 |

min Qty step size |

minNotional |

Float |

5, 25 |

10.0 |

min total order value |

retry |

int |

1, 3 |

10 |

num of order submissions |

Direct Access

execution = CSUite.mini_lot(client, symbol, size, tickSize, setpSize, minNotional, retry)

via OrderEngine Wrapper

engine = OrderEngine(client, symbol, ledger)

execution = engine.mini_lot(size, retry)

Breakeven

The Breakeven order algorithm is an algorithm which creates a mirror breakeven to an executed order, accounting for two way commission. It can enable users to instantly build and submit mirror orders to close open balances when trading net-0 strategies. To better account for the needs of algorithmic traders the algorithm contains an offset parameter which specifies an additional move of the Limit Price into a value above breakeven.

Name |

Type |

Example |

Default |

Decription |

client |

Client |

Object |

None |

API client |

symbol |

String |

‘BTCUSDT’ |

None |

Binance symbol str |

orderId |

String |

0, 1.25 |

0 |

Order qty (neg = sell) |

offset |

int |

1 |

0 |

offset from breakeven |

tickSize |

Float |

0.001 |

0 |

min tradable tick |

stepSize |

Float |

0.1 |

0.1 |

min Qty step size |

Direct Access

order = CSUite.breakeven(client, symbol, orderId, offset, tickSize, stepSize)

via OrderEngine Wrapper

engine = OrderEngine(client, symbol, ledger)

order = engine.breakeven(orderId, offset=0)